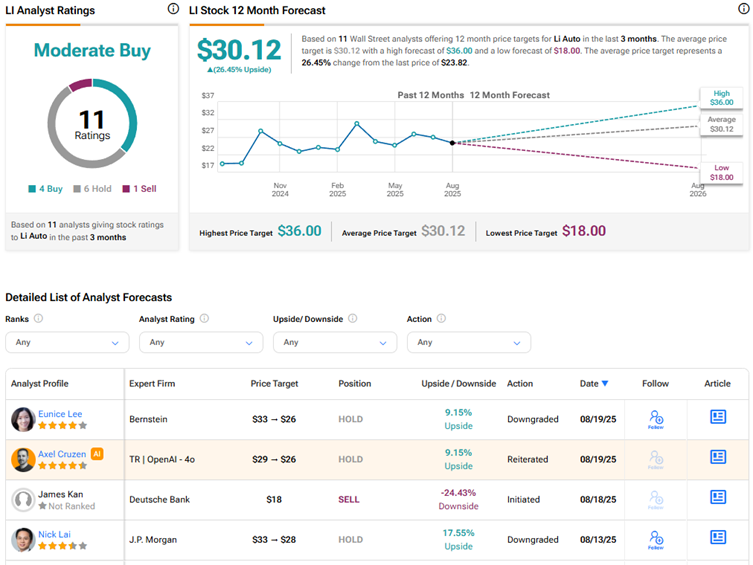

Bernstein lowered the Li Auto (Li) styles from the purchase and lowered the price target from 33 US dollars to $ 26 to reflect the ongoing challenges. The analyst Eunice Lee asserts that the technological strengths and the international growth potential of the Chinese electric vehicle (EV) maker's company remain the “competitive landscape, guaranteed a more careful 12-month perspective on Li-Auto shares. After the end of Tuesday, the Li Auto-Stock fell by 25% and was flat from year. declined by 1.1% on Wednesday.

Increase your investment strategy:

- Use Tipranks Premium with a 50% discount! Improving powerful investment tools, advanced data and expert analysts that you can use to invest with confidence.

Here is the reason why amber is careful on Li Auto Stock

Lee recognized the dominance of Li Auto in EREV technology (Electric Vehicle) from Extended Range, strong financial position, potential in overseas and considerable progress in advanced driver aid systems (ADAS). However, the 4-star analyst believes that intensive competition in the premium plug-in hybrid electric vehicle (PHEV) and EREV SUV segments as well as the challenges on the overcrowded market for overcrowded battery electric vehicles (BEV) have influenced the prospect.

In addition, Lee believes that Li Auto is a “victim of his own success in EREV”. The analyst said that the robust position of the company in Premium-Phev SUVs has increasing competition by Aito, Great Wall (GWLLF), BYD (BYDDF) and upcoming participants such as Xpeng (XPEV), Zeekr (ZK) and Xiaomi (Xiacf). In fact, the market share of Li Auto in this segment fell from 72% in the second quarter of 2023 to 34% in the second quarter of 2025. Especially after annual growth of over 100% for two years, the high-end prevation is almost 30%. As a result, Lee expects future growth to become moderate.

In addition, Lee found that the expansion of Li Auto into the BEV segment diluted the edges. The company's BEV expansion in particular looks like strong competitors such as Tesla (TSLA) and Xiaomi. Lee expects the gross margin of the i8 in the middle of the teen age to be below the 20% margin for its erev, mainly due to the 45 kWh larger battery. In view of these challenges, Lee reduced her sales forecasts of 2025 and 2026 by 6% and 16% as well as EPS estimates by 12% and 36%.

Lee's downgrade follows a recently carried out downgrade from buying JPMorgan via “conservative volume assumptions”.

What is the forecast for Li Auto shares?

In view of the short-term headwind, the Wall Street for Li Auto shares is carefully optimistic, with a moderate purchase consensus rating based on four purchases, six holds and a sales recommendation. The average Li share course of $ 30.12 shows an upward potential of 26.5%.

You can find more LI -Analyst reviews

Liability exclusion and disclosure port a problem