By Junaid Bray

The luxury goods industry is supported by long-term structural growth drivers. Rising wealth levels in emerging markets such as China, India and the Middle East have driven growth, supported by demand from mature developed countries such as the US and Europe. Despite long-term secular growth, the industry is subject to short-term cyclicality driven by wealth effects and consumer appetite for luxury goods, particularly among emerging luxury buyers.

From rise to slump

The Covid-19 lockdowns created a boom period for the luxury goods sector as dependent consumers, unable to travel and sitting on excess savings, bought luxury goods. Strong demand and the inflationary environment led to aggressive price increases by luxury goods companies.

The subsequent consumption downturn, exacerbated by high inflation and higher interest rates, as well as several years of excessive price increases, led to a decline in demand for luxury goods, partly due to reduced affordability, particularly among emerging luxury consumers. This was exacerbated by the dramatic downturn in China, which has been the strongest growth driver for luxury goods over the past two decades. China accounts for around 20-30% of luxury demand from larger luxury goods companies.

The winners emerge when the tide recedes

As Warren Buffett famously said, “It's only when the tide goes out that you realize who's been swimming naked.” The downturn has separated the higher-end luxury companies from their weaker competitors. Hermes and Ferrari are examples of luxury companies of the highest quality where demand continues to exceed product supply, which is a sign of true luxury. (Although Ferrari is an automobile manufacturer, it has more in common with luxury goods companies than a typical automaker.)

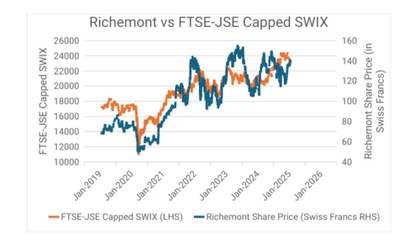

Richemont: proof of resilience

Richemont, which has a secondary listing on the JSE, has also demonstrated the high quality of its core jewelry business, which accounts for over 80% of group profits. Although Richemont's specialized watchmaking division recorded a sharp decline in sales and profits, the jewelry houses showed resilience. The core brands that many will be familiar with are Cartier and Van Cleef & Arpels.

Balancing risk and return

Due to the cyclicality and high beta nature of the sector, the sector tends to be volatile, which creates opportunities for investing in great companies. Given high margins and strong cash flows, the larger companies are considered high quality and tend to trade at premium valuations, with price-to-earnings (P/E) ratios typically above 20x. With quality companies you have to be wary of overpaying and we have seen many examples of fallen angels. (The high P/E ratings may remain, but when earnings are downgraded, stock prices tend to follow suit.) The sector tends to overreact to industry news, and we have taken advantage of sell-offs that we thought were overblown to gain positions in it to build Richemont in our funds, as we did at the beginning of 2024. This has resulted in generous returns and alpha for our clients.

We continue to monitor the sector for opportunities to invest in companies that are of high quality and offer an attractive risk-reward profile.

Junaid Bray is a portfolio manager at Laurium Capital and part of the PPS Stable Growth Fund investment team

ANNUAL REPORT