Tim Rynott, CEO from Four Corner's Helium LLC, discusses the journey of interest and investments in US helium, from an increase to a waiting game.

For some US helium investors, their self -confidence has cooled down. Will this shift shift – or exist? For too many investors, the business has expanded from delicious to eyebrows. An expensive learning curve with a thread: wait.

- Waiting for permission.

- Waiting for a rig.

- Waiting for a test.

- Waiting for income!

Early investors who have driven on AIM, TSX and ASX exchanges in warehouse multipliers are looking for encouraging news – anchored transparency. Instead, the US helium industry has started to resemble deep water oil and gas, where the return (Return on Investment) rules the day, while a robust return (Ror) is still heavy.

The early buzz

- Four main lack in just 19 years.

- Average helium price in less than a decade.

- US federal helmet reserve, supplier of ~ 30% of the domestic offer, is now exhausted ~ 90%.

- The legal processes increased by the law on inflation reduced semiconductor growth forecasts could record demand growth of 6 to 10% per year.

The basics remain: Helium is in critical technologies, environmentally friendly and yes – infitating toddlers for the coming years.

Rori realities

As an example, privately capital -centered North American helium sacrificed the early income by initially utilizing capital into his middle stream. Name this a “trust agreement” between capital providers and management. Eleven years later, near ~ 170 million cubic feet per year – almost 5% of the North America offer. But this model is special and unique. Public dealers rarely share such patience.

For most explorers:

- Midstream is not quick or cheap.

- The proximity of the pipeline to helium plants is ideal, but rare.

- Mobile facilities mean thin margins when renting it and a direct purchase Kanks the Ror.

- Flat reservoirs (800-1200 FT) have problems with low press → low installments.

- The high pressure of the subsidel results in a higher flow (50–250 mcfD), but drilling and completion can cost $ 6 million to USD $ 15 million per well.

- In Montana/Saskatchewan/Alberta tempting high -nitrogen -containing games are more affordable, but type curves indicate relatively steep declines after the first two years of production.

ROI: seal the deal

All episodes in principle occur if the expulsion rate from the source exceeds the rate of the sealing culveration, since helium can diffuse through practically all underground materials over geological times – even inappropriate granite.

It was determined worldwide that the evaporation formations with low permeability (salt, anhydrite and plaster) generate the best seals not only for oil and gas, but also for helium. It was also stated numerically that violations of the top exploration risk of oil, gas and the top risk of exploration remain helium. Breached or “blown seals”, which are often obtained with regard to tectonics, micro or transferring errors, can also be difficult with available exploration tools. In view of the fact that it can take hundreds of millions of years to fill a helium reservoir (radioactive decay is drops, drops, drops), an episodic event can destroy the economic party. Ie – destroy the ROI.

In the future, test tools/practices that are supported in reducing blown seals are:

- Pora pressure diagrams

- Paline -spastic mapping

- Borehole image protocol

- Isochronous and isopachen

Secondary exploration risks – Source, rock mechanics (porosity/permeability), migration effectiveness and trap/timing – can be with a relatively quantifiable Proximally analogous and sufficiently seismic.

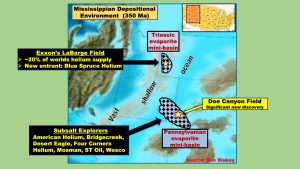

A first -class, modern analogue, Doe Canyon Field in SW Colorado, is located on the eastern flank of a massive old flat ocean (Fig. 1). Doe's Mississippian Porous Dolomites by doe – draped by a 12,500 square mile Pennsylvanian Evaporitic Canopy – almost 3 billion cubic feet have been produced by a further 4 to 6 billion cubic foot. With the river rates of more than 20 million cubic per day at 0.4 to 5% helium (almost 3% near 4 corners) and extensive flat, flat uranium/thorium -ancient basement, the 4Corner area has become suitable for cheap ROIS.

Maximizing ror

Four Corner's Helium, LLC expects port pressure diagrams and high -resolution isochrons to be used in the pinch of large evaporation bodies. The ultimate goal is to test reservoirs with an evaporation seal that is thick enough to catch a tiny helium element (not confused with molecules), while they are thin enough to avoid a 7-inch intermediate shell-a prerequisite for the borehole stability due to thick evaporators. The requirement of a 7-inch intermediate cover for today's steel prices doubles the drilling/completion capital for subalt locations and hammering the return.

Second, stacked games are also important: the seismic inversion can remove flatter oil zones via helium deposits. Oil cash flow offsets heliums notoriously slow hook -u -ups.

Supply/demand fulfills the ROI

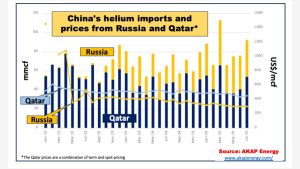

Current helium veterans-hoft oil and gas refugees who have survived (or not) through cyclical transmission scenarios, how) knowledge of how raw material price fluctuations can brutalize the Ror/Roi. A typical example: Russia's infiltration of the Chinese market share in September 2023, China shortened by over 40% in the China of Qatar and lowered the point prices of Qatar by ~ 20% within 19 months (Fig.2). The red flags of the United States are being raised!

The Amur trains from Gazprom are 1, 2 and 4 online, with 3, 5 and 6, which may be online later this year. As soon as Amur was fully equipped, it could possibly deliver 3 to 3.5x more than for non-placed Asian/Neith-East markets (including China, India, United Arab Emirates, Saudi Arabia, Vietnam, Malaysia).

If Gazprom absorb these countries that increase domestic allocations and build strategic stocks for intra pillows or future price optimization-and still have remaining capacities, what will come next for this helium bonus?

FirstFinally, the sanctions could be canceled and the market options could be expanded.

Secondand paraphrased Phil Kornbluth Kornbluth and Associates: “… the Russian helium sanctions divide a previously global helium business into two companies: those companies that can buy reduced Russian helium, and those companies that are forbidden to buy reduced Russian helium.” In this sense, how is this related to the other highly consumed, legally accessible countries?

- Japan and South Korea represent strong ~ 36% of Asia's demand, but ride a slippery slope. None of these countries has specific sanctions that prohibit the Russian helium, even though they are firmly in line with the G7/US-EU camp. In other words, South Korea has to express allies and at the same time keep industrial lifestyle open if sanctions do not bite.

- A sanction -free United States, the largest helium consumer in the world, would undoubtedly be in the Russian crosshairs. Although there are obstacles:

- Costly shipping.

- Civil unrest of many plebejers.

- The primary US dealers (air products, linden, knife, matheson, etc.) can hesitate due to the risk of reputation.

- Complex tariffs. In this case, exclusions in column 2 can lead to Russian helium being exposed to high tariffs – and effectively clear it out of the US competition.

- In the USA, Gardner is excluded from Russian -filled helium containers. Gardner in the United States delivers the vast majority of global 11 km iso-iso-isos, but Chinese companies move quickly to meet the needs of Gazprom.

- Competitive Rors/Rois – An area in which American explorers can control their own fate. The capitalism-controlled scientific ingenuity, sweat and determination can move the economy at the field level at the field level, which can be baked through which Gazprom?

Geology rules

Mother Nature rules the day again. Of 195 countries in the world, the geological conditions for commercial assistance have primarily occurred in only five countries.

In 2021, the United States Geological Society (USGS) is estimated in its well -known reservoirs that 306 billion cubic feet are recoverable. If less than 25% of this amount are classified as economically, this volume produced could meet the needs of the United States for a generation.

Top Us Helium Explorers – Namely Avanti Helium, Blue Spruce, Desert Eagle, Exxon, Four Corners Helium, Helix Resources, Mosman Oil and Gas, US Energy, and WESCO – Bring A High Level of Expertise and a Scientific Arsenal of Exploration Tools, Including Seismic Attributes Search AS AVO (Amplitude versus offset), RMS (Root Mean Square), Spectral Decomposition, Inversion, coherence, seismic petrophysics as well as high-resolution hole protocol, NMR and borehole image protocols and extended geochemistry. There is a reason why many countries around the world are looking for the specialist knowledge and tools of the US Explorationists.

It was written that modern Homo sapiens have been roaming the earth for about 300,000 years, but Helium was only discovered 157 years ago! So, investors, keep your British initiated – this new industry will have growing pain. And a waiting game!

Please note that this article is also displayed in the 24th edition of our quarterly publication.