Your shoes are certainly different styles, but the business of Deckers outdoors(Nyse: deck) And Crocs(Nasdaq: Crox) are not wild differ from each other. Every company sells shoes, both directly and through wholesale channels. But the similarities extend.

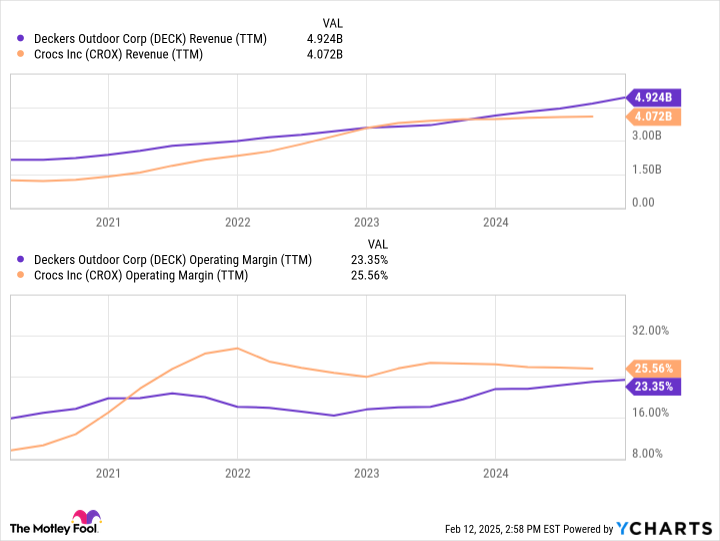

Crocs reported finance results for the fourth quarter of 2024 on February 13, so that his final numbers are not reflected in the following table. For 2024, however, Crocs had sales of over 4.1 billion US dollars. In turn, Deckers has another quarter in the 2025 financial year, but for the entire financial year it expects net sales of 4.9 billion US dollars. Therefore, deck and crocs are similar in scale.

Where can you invest $ 1,000 at the moment? Our team of analyst has just revealed what they think are they 10 Best stocks Buy now. Learn more “

Decker and crocs are also similar in relation to profitability. For 2024, Crocs had an operational margin of around 25%, which is excellent. But Deckers is not far back: a operational operating range of 22% for the 2025 financial year expects.

TTM data (Deck Revenue) from Ycharts.

At the moment, the stocks of Deckers and Crocs have returned by 30% of their 52-week heights. Which of these two shoe stocks is the case is the better purchase today?

The case for Deckers

In the investment world, growth is not the only important thing you can think about. But its meaning cannot really be overrated. Studies have shown that sales growth consistently is the biggest factor for stocks that surpasses S&P 500(Snpindex: ^GSPC). And Deckers had better growth than crocs.

In fact, growth for crocs has almost disappeared. The turnover of 2024 of 4.1 billion US dollars only increased by 3.5%compared to 2023, since the headwind of sacking sales for its other brand, Heydude, was stopped. And for 2025, management expects the sales of 2.5%at best.

In contrast, Deckers grew. In the first three quarters of his fiscal year 2025, sales increased by 19% compared to the comparable period of the 2024 financial year. Management expected to achieve growth of 15% throughout the year, which is increased by the continued robust growth rates for its two largest brands : Ugg and Hoka.

Another thing in favor of the deckers is the balance. To be clear, the balance for crocs is very manageable, as I will explain. But Crocs still has more than $ 1.3 billion in borrowing, while Deckers are debt-free. In short, Deckers have more financial flexibility.

The case for crocs

As much as it looks as if Deckers shares could be a good investment, I think that the Crocs share is the better purchase today, even after it has increased by 24% according to its quarterly report. And I don't think it is only close how I will explain.

There are some weak signals that indicate that the growth of the deckers is slowed down. According to the management of the management, sales of the fourth quarter in the financial year expect around $ 940 million. That would actually be due to sales of 960 million US dollars, which it had in the fourth quarter of the fourth quarter of 2024. In addition, its guidelines implant a lower gross margin in the fourth quarter. This could mean that prices should be reduced to promote sales. But it still expects to fight with growth.

In this light, Crocs' view of 2% growth does not look that bad.

In other words, the growth rates for Decker and Crocs could converge. And I have already found that the operating range is approximately the same and that no company gives a clear advantage. From the point of view of the investment, the Crocs share is far cheaper and acts with less than 8 -fold profits (remember that the following diagram is not updated to reflect the Q4 result of crocs):

Deck PE ratio data from Ycharts.

Based on the management guidelines, Crocs should achieve 1 billion US dollars in operating results in 2025. In comparison, the market capitalization is only 6 billion US dollars. Based on the money it has already achieved, and the profits that it expects, it could possibly pay its debts completely in 2025 if it wanted. I doubt that it will be so, but the point is that the debts is not a problem.

Crocs will probably pay part of it. After all, it paid back 323 million US dollars in 2024. But it will be more likely to return a lot of cash to shareholders with share purchases. It is currently authorized to buy a value of 1.3 billion US dollars back, which could now buy breathtaking 21% of its shares. If management decides to be aggressive to its currently cheap share price, this could increase the shareholder value in a hurry.

As you can see, Crocs' business is stable and its profit margins remain excellent. And with its current rating, it is simply too cheap to ignore. Compared to Deckers shares, I believe that the Crocs share is a much more convincing purchase today.

Don't miss this second chance of a potentially lucrative opportunity

Do you ever feel that you have missed the boat when buying the most successful stocks? Then they want to hear that.

In rare cases, our experienced team of analysts A gives A “Double Down” Stock Recommendation for companies from which you believe you have a poping pop. If you fear that you have already missed your investment chance, the best time is to buy before it's too late. And the numbers speak for themselves:

- Nvidia:If you invested 1,000 US dollars when we doubled in 2009, you have doubled.You would have 360,040 US dollars!!*

- Apple: If you invested 1,000 US dollars when we doubled in 2008, you have doubled. You would have 46,374 US dollars!!*

- Netflix: If you invested 1,000 US dollars when we doubled in 2004, You would have $ 570,894!!*

At the moment we spend “Double Down” an arms for three incredible companies, and there may be no further chance so soon.

Learn more “

*Stock consultant returns on February 3, 2025

Jon Quast has positions in Crocs. The Motley Fool has positions in and recommends Deckers outdoors. The colorful fool recommends crocs. The Motley Fool has a disclosure policy.